Before you commit capital to a growing system, you need to understand one thing most articles get wrong from the first paragraph. CEA is not a competitor to hydroponics. It is the house that contains it.

This distinction matters more than it sounds. Founders who conflate the two often make technology decisions based on a false binary, “CEA vs. hydroponics”, when the real question is which type of CEA makes sense for their crop, market, and capital structure. Investors who miss the distinction misjudge market sizing. Suppliers who market to the wrong layer of the stack lose deals they should have won.

This article is the one you read before you make any of those calls. It explains what each system is, who is actually using it at commercial scale in 2026, what it costs, and most importantly, what kind of farm it fits.

1. First: What CEA Actually Means

Controlled Environment Agriculture, or CEA, is not a growing technique. It is an umbrella term for any system that manages the variables plants care about, such as light, temperature, humidity, CO₂, and nutrients, inside an enclosed or semi-enclosed space.

Everything else in this article sits underneath that umbrella:

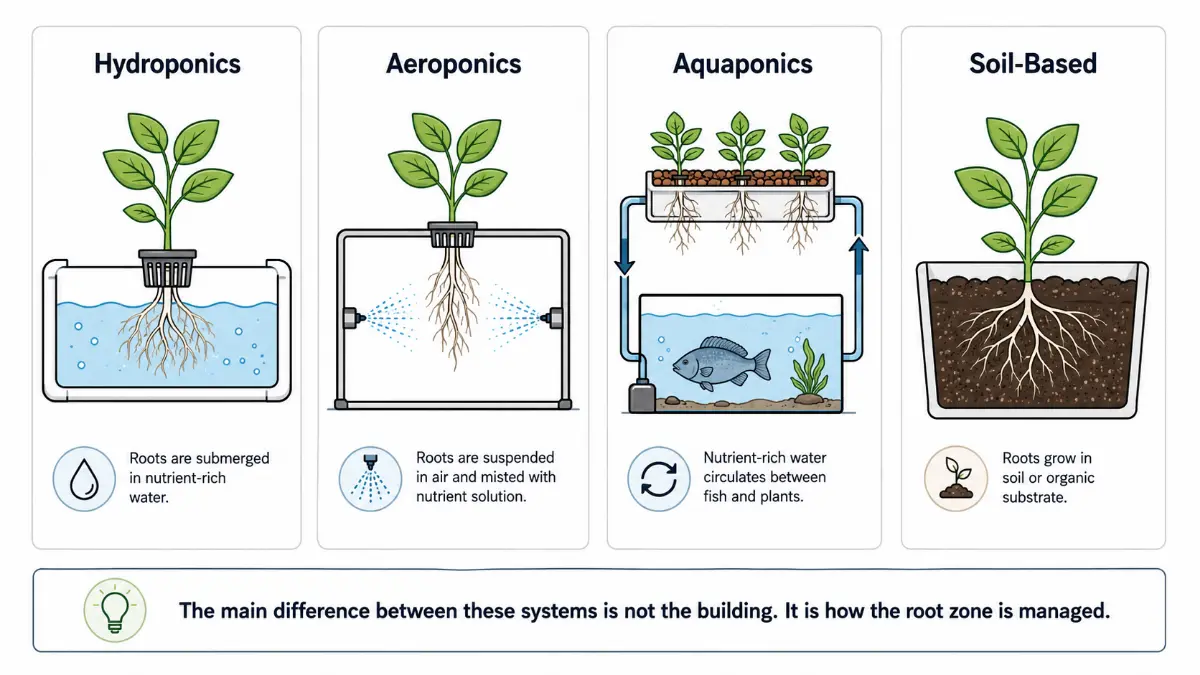

- Hydroponics, plants grown in nutrient-rich water solutions without soil

- Aeroponics, roots suspended in air and fed by a fine nutrient mist

- Aquaponics, plants and fish in a shared nutrient loop

- Soil-based indoor growing, organic substrate in a controlled environment

When a market report says the global CEA or vertical farming market is growing rapidly, it may be counting very different production models under one umbrella: hydroponic vertical farms, aeroponic systems, greenhouse tomato operations, aquaponic projects, and soil-based indoor farms. When a pitch deck says “we use CEA technology”, it tells you almost nothing about the actual growing system.

The confusion is persistent and expensive. The rest of this article uses each term precisely.

2. Hydroponics: The Industry Standard

Hydroponics is what most vertical farms actually run. It is the default choice for a reason: it works, it scales, and the supply chain to support it is mature.

How it works: Plants grow in an inert medium such as rockwool, coco coir, or perlite, or directly in a channel. The roots are continuously or periodically supplied with a pH-balanced, nutrient-rich water solution. There is no soil. All nutrition is delivered through the nutrient solution, which means precise control, but also full responsibility for getting the formula right.

The main variants:

- NFT, Nutrient Film Technique: A thin stream of nutrient solution flows continuously over roots in angled channels. It has low water volume, works well for leafy greens, and is widely used in commercial hydroponic production.

- DWC, Deep Water Culture: Roots are suspended directly in oxygenated nutrient solution. It uses more water than NFT, but can be productive and relatively forgiving.

- Ebb and Flow, or Flood and Drain: Trays flood periodically and then drain. This system is more forgiving for beginners, but often less optimized for ultra-high-density commercial production.

- Drip: Nutrient solution is delivered directly to the root zone via drip emitters. It is versatile across crop types and common in larger greenhouse operations, especially for fruiting crops.

Who uses it: The majority of commercial vertical farms operate some variant of hydroponics. Gotham Greens describes its greenhouse system as hydroponic and based on Nutrient Film Technique. Village Farms International, one of the largest CEA operators globally, also operates hydroponic greenhouse systems. The commercial standard is NFT or DWC for leafy greens and herbs, and drip systems for fruiting crops such as tomatoes and peppers.

The numbers: Market reports generally place hydroponics as the largest growing-mechanism segment in vertical farming, although exact share estimates vary by research provider. Recent market estimates place hydroponics in the low-50% range of the vertical farming market by growth mechanism, while other reports put the share closer to 60%. Hydroponic systems are also commonly promoted for using significantly less water than conventional field farming, while remaining less technically complex than aeroponics.

Advantages:

- Proven at scale across many commercial operations

- Well-understood failure modes

- Lower CAPEX than many aeroponic systems

- Robust supplier ecosystem for nutrients, equipment, sensors, and design consultants

- Applicable to a wide range of crops

Disadvantages:

- Pathogen risk: a disease in the nutrient solution can spread through the system rapidly

- Water volume creates runoff and nutrient-management requirements

- Organic certification remains controversial in some markets and production models

- Usually less water-efficient than aeroponics

Cost profile: Hydroponics is usually the lowest CAPEX entry point among high-tech CEA systems. NFT and DWC setups are well documented, equipment is widely available, and the operational knowledge base is much deeper than for newer or more specialized systems.

3. Aeroponics: The High-Performance Option

Aeroponics is the technology many people picture when they imagine the future of vertical farming. The reality in 2026 is more nuanced. Aeroponics can be highly efficient and technically impressive, but it demands more from the team that operates it.

How it works: Plant roots hang suspended in a dark chamber and receive no growing medium. At precisely timed intervals, typically every few minutes, nozzles spray a fine mist of nutrient solution directly onto the root zone. Because roots are exposed to air between misting cycles, oxygen availability at the root zone is higher than in most water-based systems. Plants can respond with faster growth and efficient nutrient uptake, depending on crop and system design.

High-pressure vs. low-pressure: Commercial aeroponics often uses high-pressure systems that atomize nutrient solution into fine droplets. Low-pressure systems are available for hobbyists and small setups, but they do not always deliver the same performance characteristics as high-pressure aeroponics.

Who uses it: AeroFarms is one of the most widely known aeroponic operators, focused historically on leafy greens and microgreens. LettUs Grow in the UK is a notable aeroponic system provider and has published comparative claims around crop-growth performance. In the Middle East, AeroFarms also established its AGX research and demonstration facility in Abu Dhabi, positioning aeroponics as a relevant technology for water-scarce environments.

The numbers: Aeroponics is often promoted as one of the most water-efficient CEA systems. AeroFarms, for example, states that its aeroponic growing system uses up to 95% less water than conventional field farming. In addition to water efficiency, some aeroponic system providers report faster crop growth compared with hydroponic baselines, but these figures should be treated carefully. Performance varies by crop, misting design, nutrient strategy, lighting, climate control, and operator skill.

For that reason, aeroponics should not be evaluated only by headline claims such as “95% less water” or “faster growth”. The stronger commercial case is more specific. Aeroponics makes the most sense where water scarcity, high-value crops, faster crop cycles, shelf-life advantages, or R&D use cases can justify the higher technical complexity and CAPEX.

Advantages:

- Strong water-efficiency story, especially in water-scarce markets

- High oxygen availability at the root zone

- No growing media, which can reduce media waste and media cost

- Potential for faster crop cycles in specific crops and system designs

- Strong differentiation story for premium markets, research, and specialty crops

Disadvantages:

- Higher CAPEX than many hydroponic configurations

- Misting nozzles require maintenance and can be prone to clogging

- Critical failure vulnerability: if misting stops, roots can dry out quickly

- Backup power and monitoring systems are not optional at commercial scale

- Higher operational complexity and more technical skill required

Cost profile: Aeroponic systems usually require a CAPEX premium compared with simpler hydroponic systems. Operating costs depend heavily on electricity, pump design, filtration, nozzle maintenance, crop cycle, and system uptime. The payback case improves where water savings, faster crop cycles, premium crops, or R&D value outweigh the added complexity.

4. Aquaponics: Niche but Real

Aquaponics integrates fish cultivation with plant growing in a shared biological loop. Fish produce ammonia waste, bacteria convert it to nitrates, plants absorb the nitrates, and the filtered water returns to the fish tanks. When it works, it works elegantly.

Why it is hard to scale commercially: Managing two biological systems at the same time is demanding. Fish require different environmental parameters than most crops. A disease event in either system can cascade to the other. Organic certification questions around fish feed complicate positioning. Labor per pound of output can also be high.

Where it succeeds: Local premium markets, farm-to-table restaurants, educational facilities, and community agriculture projects. In these contexts, the “living ecosystem” story resonates, and output volume expectations are lower.

In a 2026 commercial context: Aquaponics is not a serious competitor to hydroponics or aeroponics for most farms planning to serve retail at scale. It remains a compelling model for specific niches, and those niches are real. But if you are evaluating technology for a commercial vertical farm, aquaponics is unlikely to be the default system.

5. Soil-Based Indoor Growing: The Contrarian That Works

Here is the approach that confuses people who have absorbed the standard “vertical farming = hydroponics” narrative: growing crops indoors in living soil. No nutrient solution. No water circulation system. Just well-managed organic substrate in a controlled environment.

The main example: Soli Organic, formerly Shenandoah Growers, has built one of the best-known commercial indoor organic, soil-based growing models in the United States. The company grows culinary herbs and leafy greens across a nationally distributed network and has positioned itself around a “biology first, technology to scale” philosophy.

Why it works: Soli Organic’s soil-based system uses a closed-loop nutrient approach and organic positioning that differs sharply from most hydroponic and aeroponic models. This matters because organic positioning can command a meaningful retail premium, while also giving soil-based indoor growers a simpler story than soilless CEA systems.

The 80 Acres merger: In August 2025, 80 Acres Farms and Soli Organic announced a strategic merger, forming a combined company operating under the 80 Acres Farms name with projected first-year revenue approaching $200 million. Industry coverage of the deal reported a national retail footprint of more than 17,000 locations and annual production capacity in the range of 15 to 20 million pounds of produce. The deal brought together 80 Acres’ automation platform with Soli Organic’s organic agronomy expertise and retail distribution network. This is a meaningful validation that soil-based indoor growing is not just a transitional curiosity. It can be part of a commercially scalable model.

Organic certification as a moat: Organic certification in U.S. CEA remains contested. Soil-based indoor farms have the clearest organic positioning because their production model fits more naturally with how consumers and many regulators understand “organic”. Hydroponic certification has been allowed in some cases, but it remains controversial. Aeroponics has faced even stronger resistance from organic standards bodies. For soil-based indoor growers, that clarity matters commercially. They can tell a simpler organic story, avoid some of the policy uncertainty around soilless systems, and compete in a retail category where organic herbs and greens often command significant price premiums. This is a structural advantage, not just a marketing detail.

Energy: Soil-based systems do not require the same pumping infrastructure as hydroponic or aeroponic systems. Their energy profile can therefore be lower in some configurations, though the space efficiency is also usually lower than stacked hydroponic or aeroponic systems.

6. What the Industry Is Actually Choosing in 2026

The technology landscape in 2026 is the result of several years of market correction. The 2018 to 2022 funding cycle rewarded scale, automation, and ambitious expansion plans before many farms had proven repeatable unit economics. When capital became more expensive and energy costs rose, that model came under pressure. Several high-profile operators, including AeroFarms’ original corporate structure and AppHarvest, went through bankruptcy or restructuring.

The lesson was not that vertical farming does not work. The lesson was that the system only works when crop choice, energy price, labor model, retail access, debt load, and technology stack fit together. What remains is a leaner, more commercially disciplined industry.

The current picture:

- Hydroponics dominates the commercial vertical farming landscape. It remains the standard for leafy greens, herbs, and many greenhouse crops because the systems are proven, financeable, and supported by a mature supplier ecosystem.

- Aeroponics is strongest in water-scarce markets, premium crops, R&D environments, and systems where faster crop cycles or shelf-life advantages can justify the added complexity.

- Soil-based growing occupies a genuine niche with strong commercial logic where organic positioning, retail premiums, and agronomic expertise are properly aligned.

- Aquaponics remains a small share of commercial output and is best suited to regional, educational, community, or premium local-food models.

Comparison Table: Growing Systems in 2026

| Hydroponics | Aeroponics | Aquaponics | Soil-Based | |

|---|---|---|---|---|

| Water vs. field | High savings | Very high savings | Very high savings | Moderate savings |

| Relative CAPEX | Baseline | Higher | Higher | Often lower |

| Complexity | Medium | High | Very high | Low to medium |

| USDA Organic positioning | Contested | More contested | Possible but complex | Clearest |

| Best crops | Leafy greens, herbs, tomatoes | Microgreens, herbs, high-value crops | Leafy greens plus fish protein | Herbs, leafy greens |

| Scale readiness | High | Growing | Low to medium | Medium to high |

| Key risk | Pathogen spread | Power or misting failure | System imbalance | Lower yield density |

| Key operators | Gotham Greens, Village Farms, 80 Acres | AeroFarms, LettUs Grow | Regional and niche operators | Soli Organic / 80 Acres |

7. Which Technology Fits Which Farm Size

Small pilot under 10,000 sq ft: Start with hydroponics, usually NFT or DWC. Equipment is well documented, failure modes are understood, and operators who are still learning the crop-to-market relationship do not need the additional complexity of aeroponic maintenance. DWC in particular can offer a forgiving learning curve with good yield potential.

Mid-scale from 10,000 to 100,000 sq ft: Hydroponics or aeroponics can both make sense, depending on crop strategy. If you are growing leafy greens for a regional retailer and margins are tight, hydroponics with automation is the sensible path. If you are targeting premium retailers with microgreens or specialty herbs and can justify the CAPEX, aeroponics may offer meaningful differentiation.

Commercial scale above 100,000 sq ft: Hydroponics with full automation is the proven model. The 80 Acres and Soli merger, Gotham Greens, and Village Farms all show that scale depends less on a single growing method and more on distribution, energy management, crop focus, automation, and retail access.

R&D and specialty crops: Aeroponics can be attractive because of its root-zone control and potential for rapid crop cycles. This makes it relevant for breeding programs, pharmaceutical-grade production, and novel crop development.

The soil-based path: If your market is premium organic retail and you have the agronomic expertise to manage living soil at scale, the Soli Organic model deserves serious evaluation. The organic positioning, natural nutrient strategy, and retail premium create a cost and pricing structure that hydroponic-only analyses can miss.

8. The Energy Variable That Changes Everything

No technology decision in vertical farming is complete without an energy analysis, and this is the point where many otherwise solid business cases collapse.

European vertical farms have been especially exposed to electricity price pressure, because fully enclosed production depends heavily on LED lighting, climate control, pumps, sensors, and automation. Lighting is usually one of the largest energy loads in indoor farming, but the exact share depends on crop, lighting design, racking density, climate strategy, and local electricity prices.

Where growing systems do differ on energy:

- Hydroponics requires circulation pumps, climate control, and lighting. The overall profile is well characterized and relatively predictable.

- Aeroponics adds misting and often high-pressure pump infrastructure. This load is not trivial, and uptime requirements are strict.

- Aquaponics adds aeration, filtration, and monitoring for the fish component.

- Soil-based eliminates much of the water-circulation infrastructure, but it may also use space less efficiently than stacked hydroponic or aeroponic systems.

The critical calculation is not which system uses less energy in isolation. The real question is what your blended energy cost per pound of produce looks like against your target price point. At high electricity prices, the margin math on energy-intensive crops becomes extremely tight. This is why technology choice must be modeled together with crop selection, local energy cost, automation level, and retail pricing.

For a detailed cost model, see our analysis of how much a mid-scale aeroponic system costs. It walks through CAPEX, opex, and break-even across three farm sizes.

Where to Go From Here

Technology choice is the last decision in farm planning, not the first. Define your crop. Identify your retail or foodservice buyer. Model your cost per pound. Then choose the system that serves that strategy.

If you are currently evaluating suppliers for any of these systems, the verticalfarming.directory lists technology suppliers across all four categories, including filtration systems, lighting, nutrient delivery, aeroponics equipment, and growing media, with direct contact information.

If you want to see these systems operating at commercial scale, the best vertical farming events in 2026 offer live farm tours and side-by-side technology demonstrations. The current event calendar is at verticalfarmingevents.com.

Related reading:

- Top 10 Vertical Farming Companies in 2026, After the Industry Shake-Up, includes 80 Acres Farms and Soli Organic case studies

- Vertical Farming Events 2026, GreenTech Amsterdam, Indoor Ag-Con, and 16 more